Extreme volatility is rattling U.S. Treasury markets in the wake of Silicon Valley Bank’s collapse and investors fear a prolonged bout of gyrations before calm returns to bond markets.

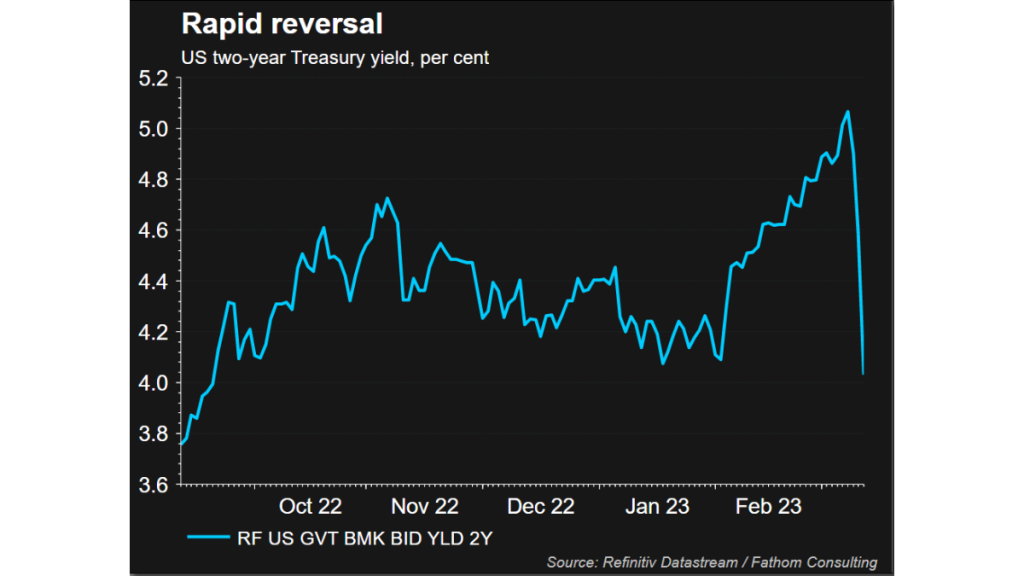

One measure of expected volatility in U.S. Treasuries – the ICE BoFA MOVE Index – has surged past its COVID-era high and now stands around levels last seen in the financial crisis. The yield on the two-year note saw its biggest one-day drop since October 1987 on Monday afternoon, while the benchmark 10-year yield fell to its lowest level since Feb. 3.

Investors had been extremely bearish on Treasuries going into last week, when Federal Reserve Chair Jerome Powell told lawmakers the central bank might have to raise rates higher than expected to cool growth and tame inflation. The Fed chief’s hawkish message helped push yields, which move inversely to prices, to their highest levels in years.

But the rapid collapse of Silicon Valley Bank as well as the fall of Signature Bank forced traders to reverse their bets on higher rates amid growing expectations the Fed would pause or slow its rate increases to avoid exacerbating stress in the banking sector. As investors piled back into Treasuries, yields plummeted.

“A bulk of market participants have not experienced a rate hike regime from the Fed nor a large bank failure, let alone simultaneously,” said David Klusendorf, chief investment officer at hedge fund Typhon Capital Management. “Expect thinner markets and greater price action until expectations become clearer how many banks are truly affected.”

He said that based on his interactions with market participants, most of the short covering came from high frequency trading hedge funds.

Hedge funds entered February holding a massive bearish – or short – position in two-year U.S. Treasuries futures, according to data from the Commodity Futures Trading Commission going back to the week ending Feb. 7.

The data has lagged by three weeks due to a cyber attack a month ago on the derivatives platform of ION Group, which has delayed trading firms’ reporting.

The short bets further lifted rates on short-term Treasuries above longer term ones, helping push a closely watched part of the U.S. Treasury yield curve to its deepest inversion since 1981.

One of the most profitable trades over the last year or so for hedge funds has been “being short global sovereign bonds to take advantage of the rise in yields as central banks fight inflation by raising rates,” said Michael Harris, president of Quest Partners, a hedge fund with $2.66 billion in assets under management.

After the big reversal in recent days, “there’s definitely been some pain for the hedge fund industry,” he said.

Michael Purves, chief executive of Tallbacken Capital, said “a huge part of the thing looks like a short squeeze,” a phenomenon in which a rising price forces bearish investors to unwind their bets by buying back Treasuries.

As of late last week, investors had largely been bracing for a 50-basis-point increase at the Fed’s March 21-22 meeting, but that hefty hike has been priced out of expectations since the SVB crisis upended financial markets. Odds of a 25-basis-point hike are about 75%, with 25% chance of no hike at the meeting, according to the CME Group’s FedWatch tool as of Monday afternoon.

U.S. banking regulators pledged on Sunday to ensure depositors at the now-shuttered Silicon Valley Bank would have access to their funds and set up a new facility to give banks access to emergency funds. The Federal Reserve also made it easier for banks to borrow from it in emergencies.

To be sure, falling yields and expectations of a more dovish Fed underpinned yield-sensitive areas of the market such as technology stocks on Monday. That helped limit the S&P 500’s losses – the index closed down only 0.15% despite sharp declines in bank shares.

Investors are awaiting U.S. CPI data on Tuesday, which some worry could force them to rethink their rate expectations once again if it shows that inflation has remained hot despite a barrage of rate hikes from the Fed over the past year.

The S&P has pared its year-to-date gains and is now up only 2.89% in 2023, after falling 19.4% in 2022.

Over the longer term, sustained rate volatility is unlikely to be good for stocks, said Purves, of Tallbacken Capital.

“If volatility in rates continues to be high, it’s going to tighten financial conditions and make it harder for equities to have a sustained rally,” he said.

NEW YORK (Reuters)

Inside Telecom provides you with an extensive list of content covering all aspects of the Tech industry. Keep an eye on our News section to stay informed and updated with our daily articles.