If you’re a gamer, then it’s a great time to be alive with all the new releases happening on almost every gaming platform; and this has been outlined by Newzoo’s new global games market report for 2021.

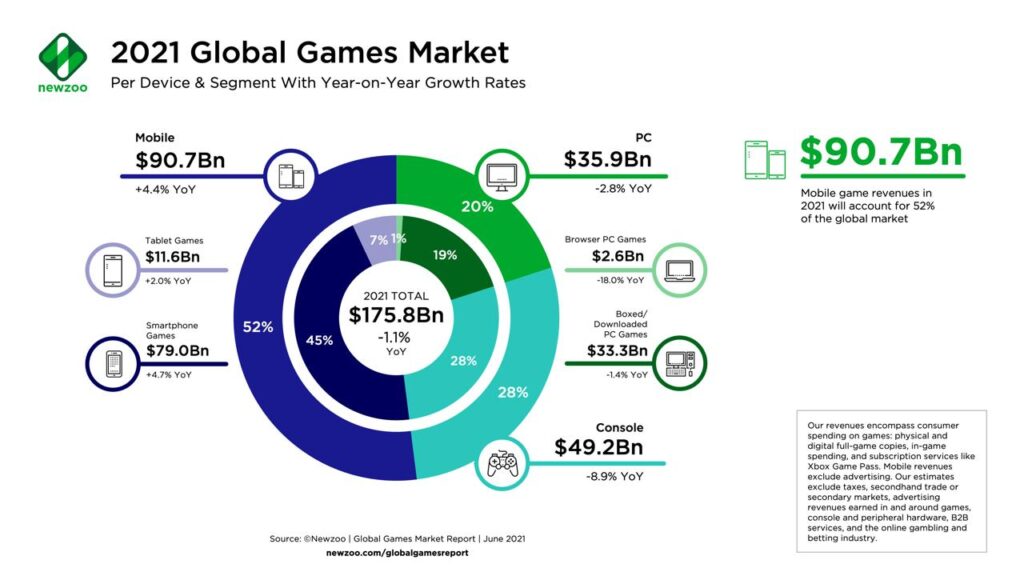

Powered by just under 3.0 billion gamers, the global games market will generate $175.8 billion via consumer spending in 2021, representing a slight -1.1 percent year-on-year decline.

This decline is caused by the PC and console market, which we forecast to decrease -2.8 percent year on year to $35.9 billion (PC) in 2021 and -8.9 percent to $49.2 billion (console), as the after-effects of COVID-19 will shape the market this year.

We forecast the mobile gaming market will generate $90.7 billion in consumer spending in 2021, growing +4.4 percent year on year. This is more than half of the global games market, as the segment is less affected by the effects of COVID-19 than PC and console gaming.

The games market’s long-term trajectory remains undeniably positive, but the market simply cannot sustain 2020’s impressive growth for another year. The market’s slight decline this year is temporary, the number of gamers is growing, and how they engage with the pastime is becoming more complex.

The metaverse trend is also accelerating at an unprecedented rate, and VR is once again blooming after a few quiet years. To that end, this year’s report features a special focus on both topics as well as our usual industry-leading market estimates, trends, rankings, and data.

The Consumers Driving the $176 Billion Games Market

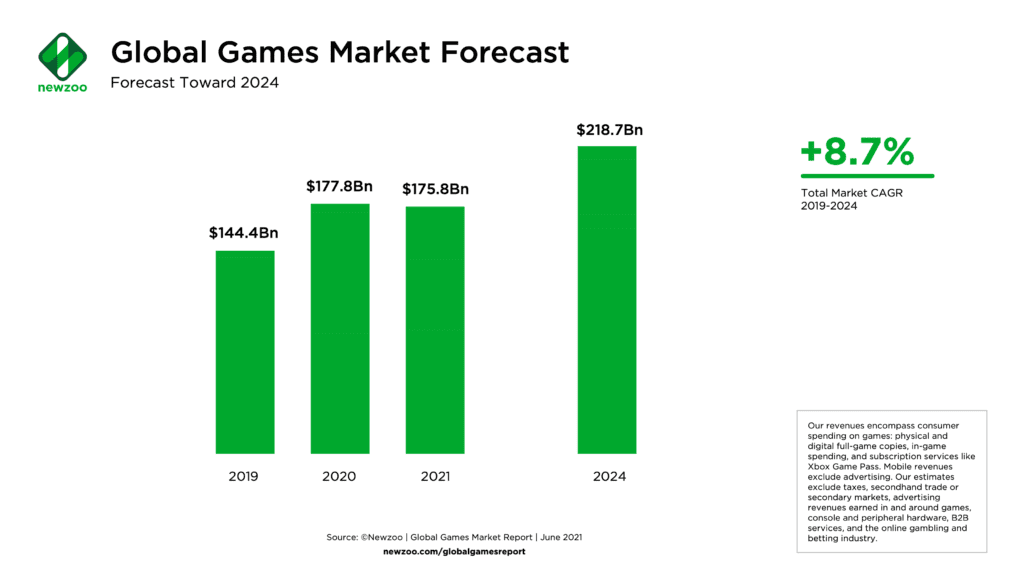

The games market will swiftly recover from its slight -1.1 percent decline this year.

The market will grow with a healthy CAGR (2019 to 2024) of +8.7 percent to reach $218.7 billion in 2024, surpassing the $200-billion threshold in 2023. But who are the almost-three-billion players driving this vigorous market?

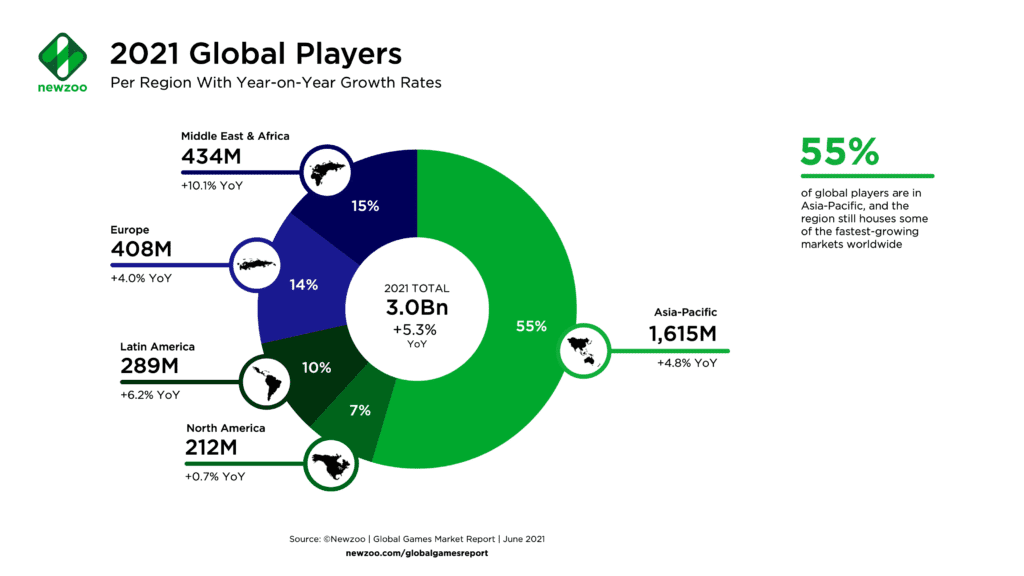

As you can see, the Asia-Pacific region by far accounts for the most players worldwide (55 percent of the global number), which makes sense as the region is home to roughly the same share (54 percent) of the world’s online population.

Asia-Pacific’s high share of players is in no small part due to the massive population numbers in China, but the region also contains growth regions such as India and Southeast Asia. Revenues paint a different picture, however.

Europe and North America heavily overindex for player spending, together accounting for over 40% of games revenues. But remarkably, the two markets house less than a quarter of 2021’s gamers worldwide (14 percent in Europe and 7 percent in North America).

Owing to the maturity of markets in these Western regions, growing revenues within them is a key challenge for publishers. This revenue saturation is why many established game companies in Europe and North America are increasingly paying attention to markets in the Middle East and Africa and Latin America.

These two regions are the world’s fastest-growing in terms of number of players. As is the case every year, the main drivers for player growth in Latin America and the Middle East and Africa are:

- Growth in their online population;

- Improving internet infrastructure;

- And smartphone and mobile internet data plans becoming more affordable.

For similar reasons, Western developers are eyeing some of the highest-potential markets in Asia-Pacific too, including China, India, and growth markets in Southeast Asia.

More than 90 percent of 2021’s Gamers Play via Mobile

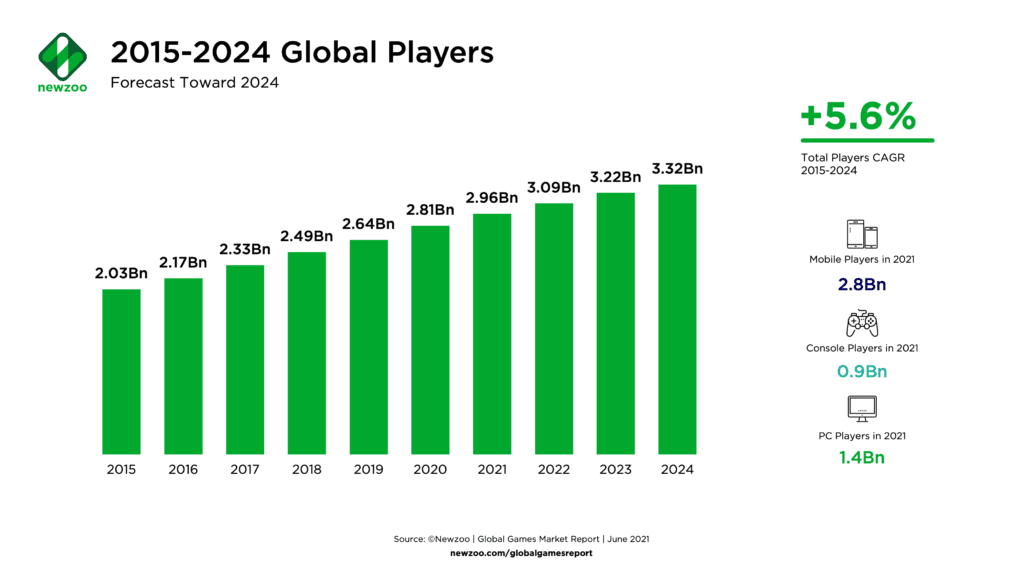

Due to Asia-Pacific’s appetite for mobile games, as well as the segment’s accessibility and ubiquity in all markets, 2.8 billion of the world’s 3.0 billion gamers this year will play on a mobile device. This is compared to 1.4 billion on PC and 0.9 billion on console.

There is understandably plenty of crossover here, as more consumers than ever before play across multiple segments. This is in part driven by the ongoing trend of platform agnosticism (blurring lines between platforms), which is in turn driven by crossplay.

More Player Growth Is Imminent

Player growth rates from 2020 to 2021 are already impressive (+5.4 percent), and many of the new gamers to enter the market during the pandemic will continue spending and engaging with the pastime. Nevertheless, even more players will enter the market.

The image above charts the player base’s impressive nine-year growth trajectory from 2015, when the player number sat at just over 2.0 billion, until 2024’s player number of over 3.3 billion.

But the ways many players are engaging with games has changed, accelerating one of the most talked-about and potentially disruptive trends in the market.

Into the Metaverse: From Sci-Fi Fantasy to Reality?

While everyone was confined indoors, the role of games rapidly evolved into something more significant than an entertainment medium.

Games have become something of an extension of our world: a key destination for social gatherings and a means to celebrate life events. Populated by digital avatars as an expression of the self, game worlds empower communities to host a wealth of social, human experiences that are unattainable via other media.

This growth of online virtual worlds—and the activities within them—has resulted in waves of attention and investment around what is commonly referred to as the metaverse.

The metaverse trend, rapidly accelerated by COVID-19, is powerful enough to persist beyond COVID-19. We believe the metaverse has a vital part to play in gaming’s future—so much so that we included a complimentary companion trend report on the topic.

Our “Into the Metaverse” report analyses:

“This future may be closer than we realize, as the pandemic has accelerated our acceptance of spending more time in virtual worlds, and Gen Z has already grown up accustomed to digital-only,” says Sébastien Borget, COO of The Sandbox.

Other Trends Driving the Games Market Today

Turning the spotlight back onto today’s games market, we expect trends like ongoing changes to tracking activity on mobile phones and transmedia experiments across TV and movies to continue rippling across the game business.

Publisher consolidation via mergers and acquisitions, continued developments in crossplay and platform-agnosticism, and challenges to store fees will also shake the dynamics of our exciting market.

We’ve analyzed all these trends and more in the full report, which also includes our first foray into VR market-sizing.

In 2020, the global Virtual Reality (VR) games market generated total revenues of $816 million via consumer spending, which is defined as VR games revenues generated through consumer VR headsets capable of 6DoF positional tracking.

This article has been written by Amsterdam-based games and esports data company Newzoo, outlining the state of the global games market in 2021, and beyond.